What is Stock Dilution?

by Capbase Staff • 7 min readpublished October 15, 2021 • updated February 26, 2026

by Capbase Staff • 7 min readpublished October 15, 2021 • updated February 26, 2026

Related

Stay ahead of the curve

join capbse newsletter

You’ll get actionable advice, comprehensive guides, interviews with founders, and more

When a company authorizes new stock, the value of existing stock is reduced. This is called stock dilution (or share dilution).

- Covered in this article:

- Why stock dilution occurs (with an example)

- Common causes of stock dilution

- Stock dilution due to SAFEs (with example)

- Anti-dilution provisions in term sheets

Why does stock dilution occur?

The easiest way to understand why stock dilution occurs is with a simplified example.

A super simple example of share dilution

Say you’re the sole founder of your company. You’ve authorized 100 shares, and purchased them. Now, you own 100% of the company.

You want to incentivize employees to join your company by offering them equity. So, you authorize 25 additional shares, and issue them to your new employees.

Now, there are 125 outstanding shares in your corporation—100 belonging to you, 25 belonging to employees.

Prior to your issuance to new employees, you owned four quarters of your company: 4/4 = 100%

But now you own four fifths: 4/5 = 80%

You now own 80% of your company, instead of 100%. And 20% of your company now belongs to employees. At the most basic level, this is stock dilution in action: You’ve “watered down” your ownership stake by introducing new stock.

Share dilution in real life

The likelihood of stock dilution playing out in the real world the way it plays out in our example is extremely small.

For starters, most founders authorize 10 million shares when they incorporate—or one million, at the very least. And those shares are each typically priced at a fraction of a cent each. And so on.

We’ll get to some more concrete real life examples of dilution shortly. But first: What events are likely to cause stock dilution at your startup?

What causes stock dilution?

In a startup, stock dilution typically occurs for one of three reasons:

- Your company authorizes more shares as part of a priced round. These shares are issued in exchange for investors’ money, in order to raise money. (The new shares fall under the category of secondary offerings.)

- Your company expands its stock option pool. During a priced round, your term sheet will specify how many additional shares you are required to authorize as compensation for future employees.

- SAFEs or convertible notes convert as part of a priced round. A priced round triggers SAFEs and convertible notes to convert, meaning you’ll have to authorize shares which you then issue to the note holders. The number of shares each note holder receives depends on how much they invested (the principal) and the valuation cap of their SAFE.

Stock dilution due to SAFEs

Let’s walk through a more complex example of stock dilution. It may be more complex than our intro example, but it’s closer to what you’ll encounter in real life as a founder.

This example takes into account:

- Your founder’s shares

- SAFEs sold to investors as part of a seed round, which will later convert to common stock

- Shares issued to an investor as part of a Series A

- The creation of an options pool as part of the terms of your Series A

Your company is called Overshare Inc.

(Your product is a social media app that uses machine learning to tell users whether their social media posts are likely to harm their future career prospects.)

You own all 8,000,000 shares in Overshare, meaning your ownership is 100%.

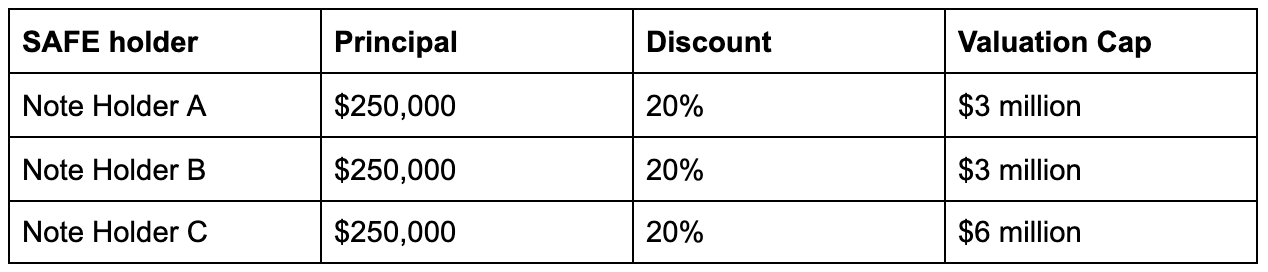

So far, you have raised money by issuing SAFEs to three investors. Each investor paid $250,000 for their SAFE. Note Holder A and Note Holder B have SAFEs with a valuation cap of $3 million. Note Holder C has a valuation cap of $6 million. They all come with a discount of 20%.

Things are going well at Overshare Inc., and pretty soon you’ve found an investor. Your investor wants to invest $8 million for 25% ownership in the company. As part of their terms, they require you to create an employee option pool worth 10% of the company.

As a result, the SAFEs you’ve issued convert to common shares.

Here’s what they look like at conversion, pre-money, before the creation of the option pool:

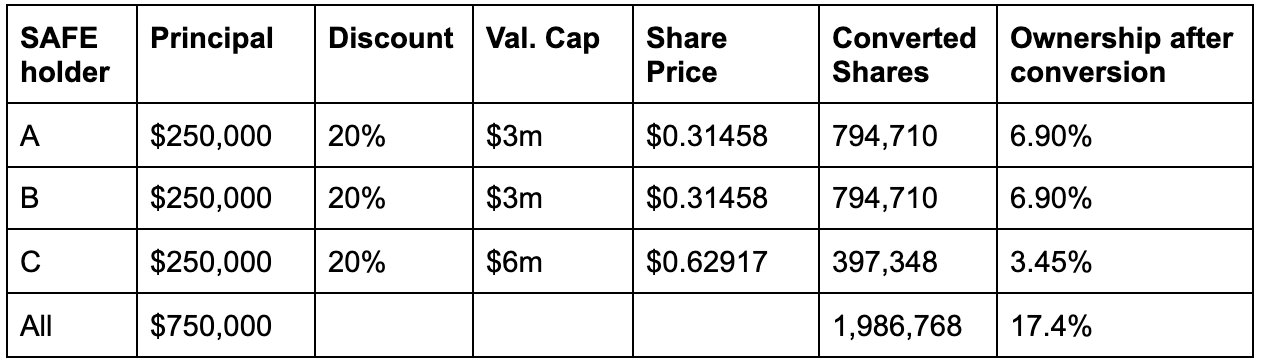

The company’s valuation is now $24 million pre-money—so the SAFE holders, with their valuation caps of $3 million and $6 million, seem to have gotten quite the deal. Even so, Note Holder C walks away with half as many shares as A and B do—thanks to having a valuation cap that’s twice as high.

Their ownership stakes are about to change, however. Once the investment goes through, the company is valued at $32 million (post-money, compared to $24 million pre-money).

The company authorizes new shares to be issued to the three SAFE holders and the Series A investor.

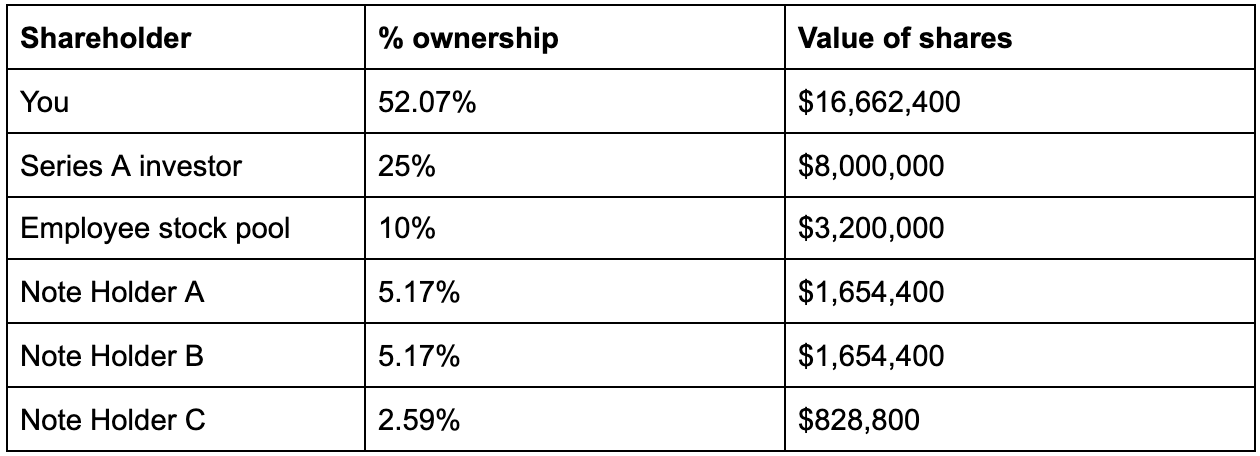

Once the dust settles, the cap table looks something like this:

You’ll notice that the ownership percentages of the note holders have decreased since they first converted. That’s an effect of dilution—your Series A investor’s purchase of 25% of the company, and the new shares authorized as a result, diluting the ownership of the note holders.

More pressingly, you’ll notice your own ownership has decreased—from 100% to 52.07%. We would describe that as a dilution of -47.93%.

Shares usually increase in value even as they are diluted

It’s important to take dilution into account when planning your company’s future—especially in terms of protecting your ownership stake, and hence the amount of control you have as a founder.

But even though it affects your ownership, dilution won’t put you in the poorhouse. In virtually every case, dilution is the result of an event that increases the value of your company—that is, investment.

So, if your ownership in your company decreases by 25%, but the company’s valuation—and the value of the stocks you hold—increases by 400%, it’s obvious you don’t need to panic about the impact on your wallet.

That being said, unless you take dilution into account and plan for it, you could still end up in a sticky situation later on, no matter how much your stock is worth. Stock dilution can reduce your ownership in the company, leading to loss of board control.

Stock dilution can be unpredictable, in particular due to SAFEs

You can see how, without careful planning, you could end up owning less of your company than you intended to, resulting in less voting power. This is especially a danger if you’re issuing many SAFEs before your first money round—particularly if those SAFEs all have differing discounts and valuation caps.

In the heat of the moment, SAFEs can almost seem like free money; your company is getting cash in the bank account, but you aren’t sacrificing ownership. That all changes when you close your first funding round, and those SAFEs convert to stock.

That’s why maintaining an up to date cap table is essential. It tells you how much of your company you’re potentially giving up when you issue SAFEs, and what kind of equity dilution a funding round may cause.

Capbase automatically updates your cap table whenever you issue SAFEs or stock, or authorize new shares. It significantly reduces your chance of making a costly mistake, and ensures you always have a grasp on who owns what.

Anti-dilution and the term sheet

On term sheets, anti-dilution provisions are designed to protect the investors’ investment against the effects of dilution during subsequent funding rounds.

Subsequent funding rounds can especially cause a problem for existing shareholders if your company experiences a “down round”—if stock price during a future funding round is less than it was previously. (Example: Series A stock is purchased for $0.75 per share, but Series B is purchased for $0.50 per share.)

To compensate stockholders for a potential down-round, anti-dilution provisions require you to authorize extra stock for these investors, effectively to make up for the fact that your stock is now cheaper than when they purchased it.

You might argue that, if a VC truly believed in your startup, they wouldn’t want to include these provisions. After all, if you’re going through a down-round, your company is already suffering; requiring you to authorize extra stock is only going to hurt you more—by increasing the effects of dilution, and diluting founders’ shares.

Whether you accept anti-dilution provisions, negotiate new ones, or reject them entirely will depend on your relationship with your prospective investor. In some ways, you can think of this like negotiating a prenup with a future spouse.

In any case, let’s take a quick look at the two main types of anti-dilution.

Absolute anti-dilution provisions

An absolute anti-dilution provision protects an investor’s investment regardless of whether your next funding round is down-round. Meaning, in any situation where your investors’ shares would be diluted, you are required to authorize extra shares and issue them to the investor in order to make up the difference.

Not only does such a provision hurt your own shares the moment you raise another round, it also turns off future investors; their own shares will be diluted when they invest.

An absolute anti-dilution provision is a red flag; if your prospective investor includes it on the term sheet, it’s time to question their motives, as well as their level of experience. If they then insist it stays on the term sheet, it’s time to cut them loose. They don’t have your best interests in mind.

Ratcheting anti-dilution provisions

Ratcheting provisions protect investors against future down rounds. There are two types: A full ratchet, and a weight-average ratchet.

In the case of a full ratchet, the investor gets a “do-over”; in the event of a down round, they can repurchase stock at the new, lower price.

Example: You have one investor, who bought $5 million worth of stock during Series A for $0.70 per share—that’s 7,142,857 shares. Your Series B is priced at $0.50 per share. Your investor now has the option to purchase $5 million worth of stock at $0.50 per share—meaning, they now own 10,000,000 shares.

Full ratchets were more common in the past—they’re rare today, and you should be hesitant to accept one on your term sheet.

A weight-average ratchet is more likely. In this case, your investor can still repurchase shares during a down round. But rather than buying them at the new price, they buy them at the weighted average between the Series A and Series B rounds.

Let’s follow our example above, but assume that Series B, like Series A, is a $5 million round—this time priced at $0.50 per share. In that case, the weighted average between the two rounds is $0.60. Your investor can repurchase stock at $0.60—they get 8,333,333 shares, rather than their original 7,142,857. Still an increase, but not as drastic as it would be with a full ratchet.

Summary

- Stock dilution is the result of new stock being authorized—typically due to an investment round

- While investment rounds will dilute your ownership in your company, they also increase its value; it’s a trade-off.

- An up-to-date and organized cap table can protect you from nasty surprises

- Be aware of dilution while issuing SAFEs—what feels like free money now could come back to bite you later on

- VC term sheets may include anti-dilution provisions, but they are never to your benefit, and in some cases could be a red flag that you should find a different investor

—

If you’re worried that issuing SAFEs now could dilute your stake later, during a fundraising round, one of the smartest steps you can take is to learn how they convert. Check out our article, How do SAFEs and Convertible Notes Convert During a Priced Round?

Written by Capbase Staff

Capbase is a team of designers, engineers, and business professionals spread across 6 time zones on 3 continents united by our passion for dogs, coffee, and great software.

Related articles

The Ultimate Guide to Cap Tables for Startup Founders

Most founders have little clue about how cap tables work when they start their first startup. Keeping accurate records of your cap table is essential for startup founders if they plan on raising capital from VCs or selling the company.

by Greg Miaskiewicz • 8 min read

by Greg Miaskiewicz • 8 min read by

by What Startup Founders Should Know About Capital Gains Tax

Explore the intricacies of capital gains tax in our comprehensive guide. Understand the difference between short-term and long-term gains, the tax rates for 2023, and the unique provisions that may apply to you, like the Qualified Small Business Stock exemption and the Alternative Minimum Tax.

by Michał Kowalewski • 7 min read

by Michał Kowalewski • 7 min readDISCLOSURE: This article is intended for informational purposes only. It is not intended as nor should be taken as legal advice. If you need legal advice, you should consult an attorney in your geographic area. Capbase's Terms of Service apply to this and all articles posted on this website.